Unlike the massive pipelines that supplied Europe’s factories and power plants, however, the energy infrastructure that connects Russia and China is still rather limited and underdeveloped. This has led to a flurry of new projects aiming to better link the two nations, and at facilitating energy exports, of which the most important is the ‘Power of Siberia 2’ pipeline which would transit straight through Mongolia, passing by Ulaanbaatar. Connecting the vast Siberian oil and gas fields with China’s northern factories and population centres, the pipeline promises to bring both potential economic opportunity and political risk to Mongolia, with important long-term consequences for Europe, Russia and China.

What is the “Power of Siberia 2” pipeline?

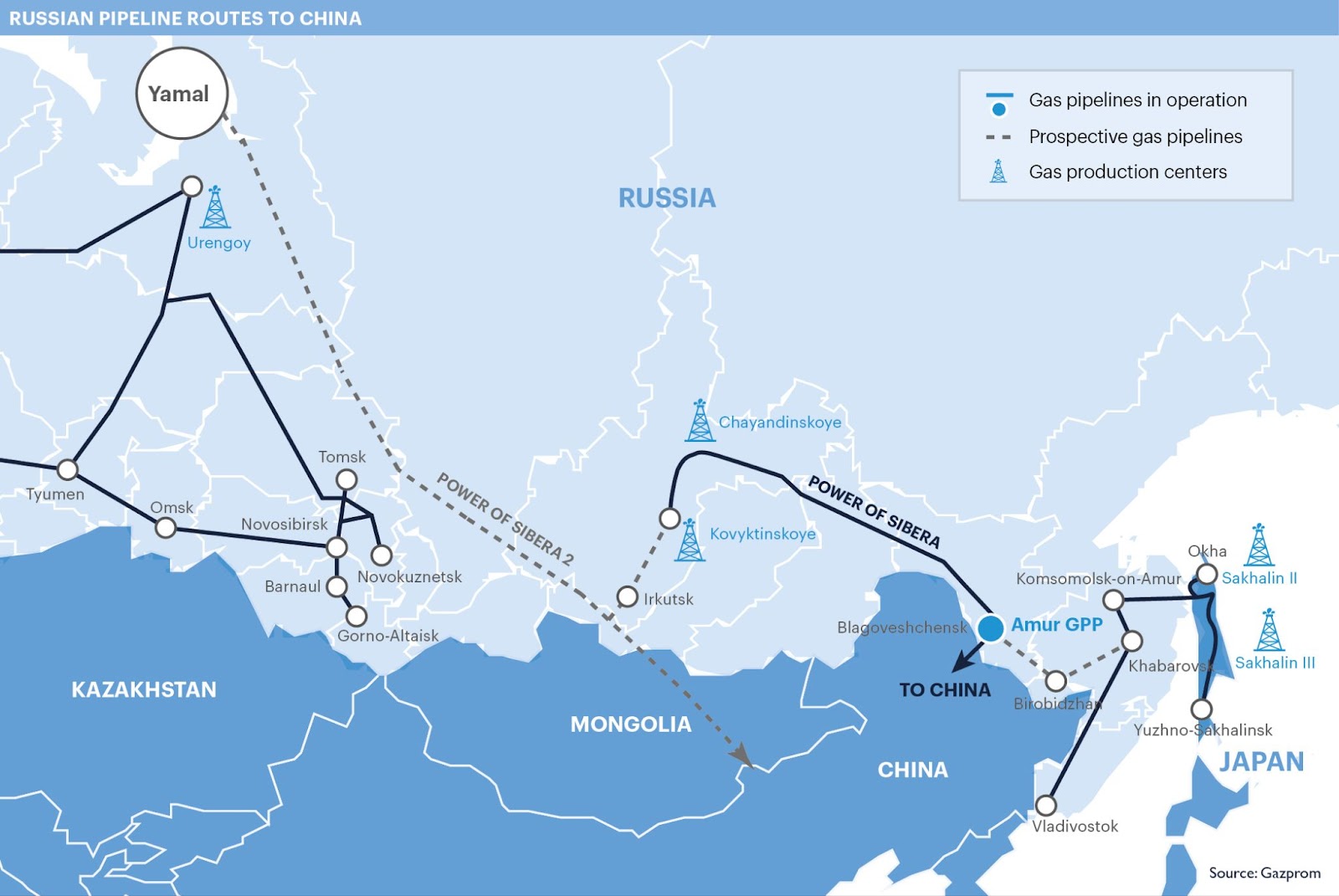

The idea of the Power of Siberia 2 pipeline was born in 2006, when Hu Jintao and Vladimir Putin agreed to an initial version of the pipeline that would transit through the Altai mountain range, where the Russian and Chinese borders briefly touch between Kazakhstan and Mongolia. The agreed upon price was to be similar to what Russia was selling to Europe in 2006. However, this concept quickly faced insurmountable obstacles that led it to be shelved in 2009. It was briefly revived in 2014 only to be postponed indefinitely in 2015 in favour of the Yakutsk-Heihe (Power of Siberia 1) pipeline. Essentially, China had signed supply agreements with Kazakhstan and Turkmenistan that provided natural gas at a cheaper price, Russia had little gas to spare from its sales to Europe, and the cost of building the pipeline through the mountainous and underdeveloped Altai region was considered too high for the potential profits that could be made at the time.

Instead, in 2012 a more limited parallel project was approved, a pipeline that would transport natural gas from Russia’s Yakutsk region to Heihe in China, supplying the Chinese north-east with gas for its important factories in the region and diversifying Chinese gas supplies. This pipeline, completed in 2019, is not connected with the main Russian pipeline network, mainly built by the Soviet Union to carry gas and oil from the deposits in central Siberia to the industrial centres of western Russia and later to its European customers. It currently carries 67 billion cubic metres per year of gas.

Despite repeated attempts by the Chinese government to gain more access to Russian natural gas, these were repeatedly denied until the start of Russia’s invasion of Ukraine. Russia’s quasi-monopolistic position in Europe as its main fossil fuel supplier allowed it to charge far higher prices compared to its other available markets, including China, where it had to compete with the gas-rich Central Asian nations. The existing infrastructure and new pipeline construction also favoured this approach, as the planning and construction of the now defunct Nord Stream 2 pipeline shows. Russia came to rely on European revenues as much as Europe relied on Russian fossil fuels for its heating and industry, a calculation that no doubt influenced Putin’s decision to invade Ukraine in 2021, expecting that Europe would passively condemn the act as it had done with Crimea in 2014.

Nevertheless, Europe’s decision to ‘switch off’ the tap and transition away from Russian fossil fuels left the country with an increasingly grave dilemma. Not only had Russia relied on the revenues from these sales to fund an important part of its budget, but with the majority of its infrastructure geared towards export to now-blocked Europe, it found itself with the need to find new markets to export natural gas, as well as the associated need to build new infrastructure to transport it. It is also important to mention that closing and reopening gas wells and pipelines is a very costly, time-consuming and potentially dangerous process, meaning that Russia also found itself under the additional pressure of finding new buyers as soon as possible or risk letting its extraction infrastructure degrade.

The combination of the factors above led to the original Power of Siberia 2 project being dredged out of limbo in 2021 to facilitate Russian gas export to China, with the overall aim of replacing European with Chinese sales. It would connect the great Siberian fields to central China while also connecting Russia’s pipeline infrastructure, which is currently divided between East and West. This time, however, the chosen route was changed to pass straight through Mongolia, joining China through the Gobi desert. Although the pipeline was supposed to begin construction in early 2024 with the aim to supply gas by 2030, construction delays have delayed the start to 2025.

Outline of the Negotiations

The negotiations and construction of the Power of Siberia 2 pipeline have been nothing but smooth. First, there was significant disagreement on the course of the pipeline, as the Chinese preferred to follow the Altai route and thus cut Mongolia out of the equation. Given that the Mongolian government has historically been far more friendly to Russia than to China, from which it seceded in 1911, its ultimate involvement can be seen as an attempt by Russia to bring a friendly party on its side of the negotiating table. Mongolia has much at stake, as the country still relies on Soviet-era coal power plants to heat its capital and its 1.5 million residents, the natural gas brought by the pipeline would bring much-needed improvements in pollution, energy cost and availability, as well as significant government revenues from transit fees but also the power to switch off the tap in the case of disagreement.

Given the limited influence Mongolia can bring to the discussions, however, it is China that holds the main power in the negotiations, given Russia’s time and budget constraints. In a test of their ‘no-limits partnership’, and with little choice on the matter, Russia has been granting an increasing amount of concessions to China. These include fronting the entire construction cost of the pipeline, estimated to be around 14 billion USD, as well as cheaper gas prices for China compared to the present. Currently, Russia is selling gas to China through the Power of Siberia 1 pipeline at 15-20% discount compared to its competitors, and the final price is likely to be even lower than that. As a result, Russian negotiators have attempted to buy time, stalling the negotiations and delaying construction in the hope of an unexpected, though unlikely, boon.

China is also in a stronger position to force Russia to agree to its demands due to the fact that it does not currently need the gas it will import. It satisfies its current energy needs by importing gas from Central Asia, where it chiefly imports from Uzbekistan, Turkmenistan and Kazakhstan. Since all other neighbouring countries to Russia in Central Asia are either gas suppliers themselves or too economically small to buy large quantities of gas, the market is effectively a monopsony where China is the only buyer. Unlike Russian oil and gas sales to Europe, where it was by far the most important supplier, Russia is competing against established sellers for the attention of a single monopsonist buyer, driving down prices even further.

Russian gas, although not needed at present, is seen in China as a way to diversify and securitize its energy supplies for the future. Most importantly, it does not transit through the strategically crucial Malacca strait or the South China Sea, where the United States Navy could intercept incoming shipments in the event of a conflict. Russian gas could also be used to replace polluting coal power plants, provide cheaper energy for industry, and serve as a strategic reserve for future economic and industrial expansion.

What will the pipeline bring to China, Russia, Mongolia, and the European Union?

Without a doubt, China will be the party that benefits the most from the construction of the Power of Siberia 2 pipeline. Although Russia will gain in being able to finally sell its currently idle gas, its selling price to China is around half of the European selling price. The lost revenues, however, are not the only important resource Russia has lost by interrupting gas sales to Europe. The strategic influence it could exercise over Europe by threatening to halt the gas deliveries that powered much of the export-driven Italian and German economies has disappeared only to be replaced by an increasing dependence on sales to China, which will become its biggest buyer of natural gas. Given Russia’s current diplomatic isolation and gradual alignment with North Korea and Iran, China’s importance in Russia’s economy will continue to grow in the foreseeable future. Although this is certain to deepen the ‘no limits partnership’ between the two countries, an increasing dependence on China will not be well perceived in Russia, forecasting a tricky balancing act for Putin.

Nevertheless, access to cheap Russian gas for China, combined with rising energy prices in Europe, holds the potential risk for the EU of exacerbating dumping from the Chinese industry abroad, as well as increased competition for European manufacturing. Given the high price of imported oil and gas from the Americas, limited domestic reserves, and instability in the Middle East, Europe currently faces high energy prices. It is crucial for Europe to continue and accelerate its green transition, especially in electricity generation, to enable its industry to remain competitive on the world market, given the importance of trade for both the EU and European economies. Failure to do so could lead to rising unemployment, which would translate to a rise in support for extremist and populist political parties, which in several European nations have already gained significant support.

Lastly, the pipeline promises to bring both risks and benefits to Mongolia. The country will gain a significant source of revenue from transit fees, up to 1 billion USD per year, diversifying away from the volatile commodities which currently make up most of its government revenues. The pipeline will bring thousands of jobs to Mongolia, facilitate its transition away from coal, and promote economic diversification and development. The construction of the Power of Siberia 2 pipeline, however, does not come without negatives for Mongolia. Firstly, although natural gas is less polluting and carbon-intensive compared to coal, the expansion of natural gas infrastructure could delay the development of renewable energy in the country, which possesses an immense untapped capacity for solar and wind farms in its southern Gobi desert. Most importantly, Mongolia, a small democracy of 3 million sandwiched between autocratic giants Russia and China, could find itself increasingly dependent on and influenced by Beijing and Moscow.

Russia could, for example, threaten to halt gas deliveries to the benefit of its own interests, or in order to influence elections or government policy. Moscow has been worried about the number of people escaping its draft by moving to Mongolia, and the increase in Mongol separatism in its eastern regions. Even more worryingly for Mongolia, the country’s independence may become more squeezed between its two neighbouring giants. Mongolia itself, however, has been broadly supportive of the project given its potential for revenue and as a vehicle to support native industry with plentiful and accessible energy as well as the power to cut off the pipeline in the event of a potential discord. Given Mongolia’s track record in balancing the interests of its powerful neighbours, as well as its growing ties to fellow democracies in the West, which it can call upon for diplomatic and financial support if push comes to shove, there is great promise for strong growth in Mongolia.

Author: Giacomo Ferri, EIAS Junior Researcher

Photo credits: Unsplash